.png)

A monthly sentiment-based reading of the AEC News

The Construction Confidence Index (CCI) provides monthly insights into market sentiment across the Architecture, Engineering & Construction technology landscape. Industry leaders, investors, and strategic decision makers can leverage these unique sentiment insights to understand market momentum, identify emerging opportunities, and time critical business decisions. Our proprietary methodology tracks not just what is happening in AEC tech — but how the industry is talking about it, revealing shifts in strategic positioning before traditional metrics reflect them.

Why Narrative Tone Matters for Strategic Decision Making

Sentiment reveals market positioning long before financial numbers do. When language around emerging technologies grows more optimistic and confident, it often signals deeper narrative shifts: rising investor interest, category maturation, or market readiness for scale.

Conversely, when tone flattens or subtly turns cautious, it can be the first visible indicator of market fatigue, regulatory uncertainty, or narrative saturation — critical signals for timing market entry, exit, or pivot strategies. Tracking the tone of the AEC news is like watching the weather of an industry. Not the climate, but the weekly winds.

How We Measure Market Sentiment

What We Track: Our AI analyzes over 2000 industry articles every month — from funding announcements to policy changes — and assigns each a sentiment score from -1 (highly negative) to +1 (highly positive).

How It Works: Advanced LLMs identify emotional undertones in industry coverage. Instead of just counting headlines, we measure confidence levels, optimism, and caution in how journalists, executives, and analysts frame developments.

What You Get: Clear sentiment scores across key dimensions

- Overall market tone plus dedicated scores for Funding & M&A and Market Expansion activities

- Regional markets (US, Europe, UK, India)

- Technology and topic trends with monthly share changes - from Government Policy & Regulation to AI, Sustainability, and emerging themes

- Strategic business activities with sentiment tracking and momentum indicators

TL;Copy

Execution > Vision. Markets continue to reward what gets built. Sentiment is strongest where outcomes are implemented — not merely imagined.

UK = Capital Conviction. The UK leads in funding headlines. Investors are betting on early-stage AI and retrofit innovation. But mixed trust remains due to policy friction.

India = Operational Momentum. India shows the highest sentiment - again. Few negative stories, and optimism comes from real-world rollouts, not promises.

AI + Safety = Lift. Themes around automation and safety continue to drive positive tone. Robotics, jobsite digitization, and applied AI remain top optimism signals.

Region = Diverging Paths. Europe edges upward with policy strength. The US rebounds slightly. India holds strong. The UK splits — investor interest meets regulatory delays.

Confidence Shifts: From Speculation to Deployment

The AEC Topic Charts in June

Government Policy continues to dominate the thematic coverage, yet sentiment remains mixed. The cautious optimism seen in sustainability, safety, and automation persists - with Input Costs & Supply Chain retaining positive momentum.

AI maintains high visibility but sentiment gains are concentrated in applied use cases, particularly when linked to jobsite safety or predictive maintenance. But in general. No big shifts.

June Sentiment: Stability, With Localized Tension

Snapshot of the Tone across this month's AEC Landscape

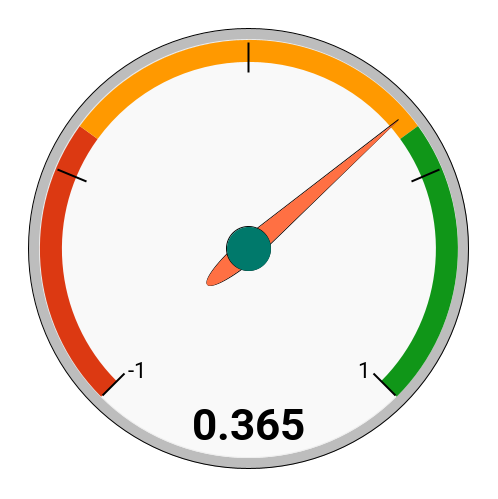

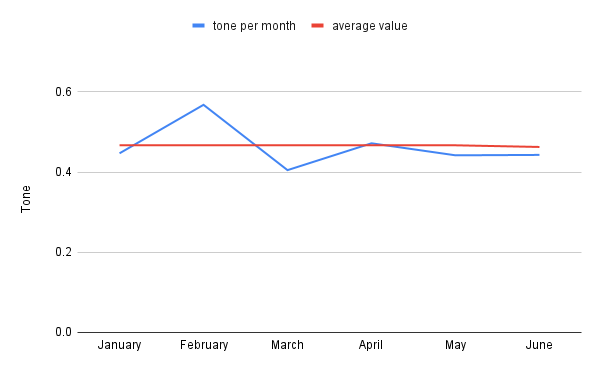

June's sentiment registered at +0.365, marking a rebound from May's +0.348 and continuing a broader trend of cautious optimism seen throughout the first half of the year. This marks the sixth consecutive month of positive sentiment, despite small fluctuations along the way.

Overall Market Tone

June's sentiment registered at +0.365, marking a rebound from May's +0.348 and continuing a broader trend of cautious optimism seen throughout the first half of the year. This marks the sixth consecutive month of positive sentiment, despite small fluctuations along the way.

How the overall Market Tone evolved over the past weeks

The overall tone has evolved from early-year enthusiasm into more grounded confidence, driven by credible growth stories and implementation momentum. Forward-looking narratives around execution, automation, and safety continue to gain traction, reinforcing a structural, not cyclical, shift in market outlook

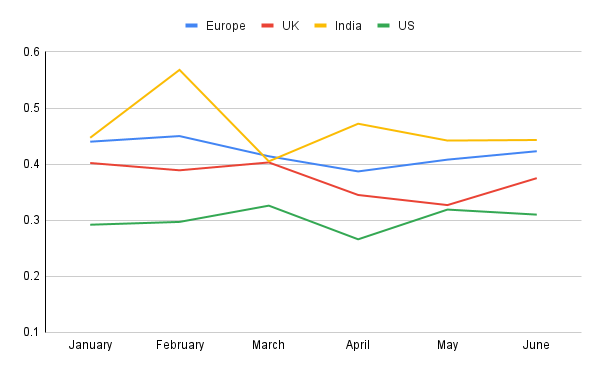

Regional Headlines: India Leads, UK Polarizes, US Cautious, Europe Climbs

Regional Sentiment Landscape

Europe UK India US

Each region’s sentiment pattern mirrors broader strategic shifts: India’s implementation-focused optimism, Europe’s structured consistency, the UK’s widening polarity due to policy friction, and the US’ cautious rebound from regulatory lows.

🇪🇺 Europe: Coordinated, Cautious, Consistent

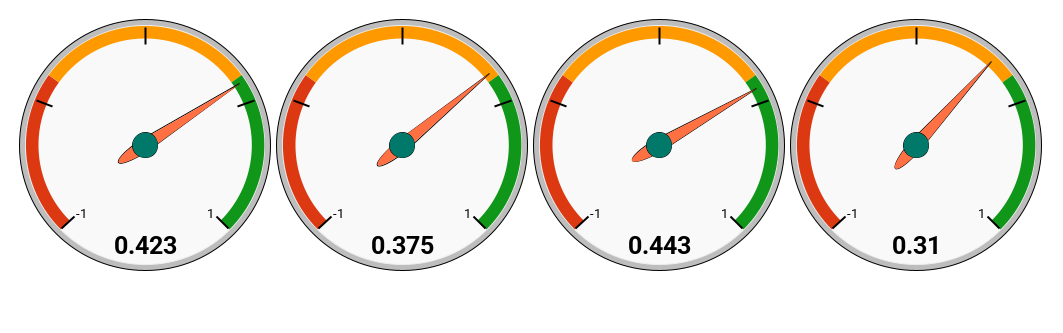

Europe's sentiment ticked up to +0.423, signaling a gradual reinforcement of policy-driven optimism. Media coverage highlighted positive developments like the rollout of EU-wide energy benchmarking regulations and advances in digital building permits. However, pushback arose around bureaucratic slowdowns - including critiques of solar infrastructure mandates in France and planning law friction in Latvia. The general tone remained constructive but not without regulatory caution.

🇬🇧 United Kingdom: Investor Energy Meets Policy Drag

The UK recorded a sentiment score of +0.375, a modest improvement from May. The rise reflects investor appetite, but sentiment remains tempered by regulatory standoffs. At the same time, the tone remained split: headlines like "Builder.ai at risk of collapse" and analysis of prolonged appeals processes in housing dominated the negative sentiment. The polarity suggests a market advancing in capital but lagging in execution clarity.

🇮🇳 India: Stability Through Implementation

India continued to lead in regional confidence, with a sentiment of +0.443 — the highest among all tracked geographies. Noteworthy articles focused on electric fleet rollouts, India's first AI-driven IT park in Thane, and hydrogen infrastructure partnerships. Regulatory announcements supporting green building and fast-tracked infrastructure approvals contributed to the upward momentum. Critical articles were few and focused mainly on implementation speed rather than strategic direction.

🇺🇸 United States: Disciplined but Lagging

The US sentiment came in at +0.310, showing a smaller rebound than expected. Positive signals came from late-stage funding rounds, like Buildots’ $45M Series D, and narrative emphasis on safety leadership and workforce digitization. However, major setbacks included stories on failed building code reforms and inconsistent state regulations, which continued to weigh down sentiment. The market shows signs of discipline, but structural fragmentation tempers investor confidence.

Regional Trajectory Comparison

What Moved Market Sentiment in June?

June’s sentiment story was shaped by a clear push-pull dynamic between regulatory strain and delivery optimism. High-impact positive headlines centered around safety, AI applications, and digital jobsite productivity, particularly in India and the US. Negative tone drivers included permitting gridlock in the UK and fragmented enforcement narratives in parts of the US.

Key sentiment movers included:

- Positive Influences:

- AI-driven safety solutions and predictive workforce analytics

- Electric fleet deployment and hydrogen infrastructure pilots (India)

- Public-private cooperation on decarbonization standards

- Negative Influences:

- Reports of permitting delays and appeals backlogs (UK)

- Conflicting regional policies and deregulation backlash (US)

- Regulatory bottlenecks in digital mapping and energy audits (Europe)

This month’s polarity across regions and topics reflects a broader trend: optimism is growing where implementation is visible, while friction remains where rules outpace clarity.

Capital Flows, Proof Wins: Market Sentiment Splits Around Execution

Funding, M&A & Market Expansion Tone

Funding sentiment in June recovered modestly to +0.332, while Market Expansion sentiment climbed to +0.540, continuing its upward trend from earlier in the year. This widening divergence underscores a fundamental realignment in how confidence is earned: capital alone no longer moves the narrative - execution does. Investors are gravitating toward companies that demonstrate rollout capabilities, regional penetration, and measurable ROI!

The UK stood out with the high funding volume, driven by a surge in early-stage activity across AI-enabled retrofit technologies and carbon-tracking platforms. Yet high volume did not necessarily translate into uniform confidence, as executional doubts persisted.

In contrast, the United States saw fewer deals by volume but significantly more conviction at the late stage. Buildots’ $45M Series D exemplifies the kind of traction-driven raise investors now favor — focused on predictive analytics and tangible jobsite performance.

India remained relatively quiet on the fundraising front, but that quiet was strategic. The lack of noise signaled a pivot from capital raising to delivery: implementation of AI solutions, electrified infrastructure, and pilot rollouts dominated the narrative.

Together, these patterns reflect a maturing ecosystem where momentum is awarded to what scales, not what speculates.

How June's growth feels compared to the others

Key Insights and Takeaways

June’s data affirms a structural shift in AEC tech: momentum follows delivery, not headlines. Sentiment continues to break away from capital hype and align more with tangible implementation.

The AEC tech market has now logged six consecutive months of positive sentiment. A brief dip in May was followed by a June rebound, reinforcing that optimism is rooted in recurring traction — not episodic excitement.

Execution outpaces speculation. The growing gap between Market Expansion sentiment and Funding & M&A shows that rollout and replication matter more than fundraising buzz. Applied AI, robotics, and sustainability — when implemented, not pitched — drive confidence.

India leads in sentiment stability. Minimal negative coverage and consistent execution stories underscore a mature, grounded growth curve.

The UK splits. It generates the most funding attention but is held back by regulatory frustration. The gap between investor excitement and institutional clarity remains unresolved.

The US shows late-stage discipline. High-value funding and jobsite safety innovation boost sentiment, though national inconsistency in codes and oversight continues to hold confidence back.

Europe climbs methodically. Sentiment remains balanced, supported by digital transformation and decarbonization frameworks. The tone is less volatile — and increasingly institutional.

Topics like automation, safety, and AI have transitioned from trend to baseline. This evolution is mirrored in coverage: away from hype and toward application.

In short: the June CCI confirms that confidence now follows credibility. Where traction is visible, sentiment sticks. Implementation is no longer an afterthought - it’s the primary driver of momentum.

Related Perspectives